I dated restored the assessment order passed by the assessing officer under section 143(3). The assessee company was in the tea business and it filed its revised return of income. The assessment was completed under section 143(3) after making certain additions. The CIT found the AO's order to be erroneous and restored the matter to me on appeal. The IDAT held that the AO had made no error in accepting the tax return, in which composite income was computed by the assessee in accordance with Rule 8 of the Income Tax Rules 1962. It showed the assessment order passed by the assessing officer under section 143(3).

Award-winning PDF software

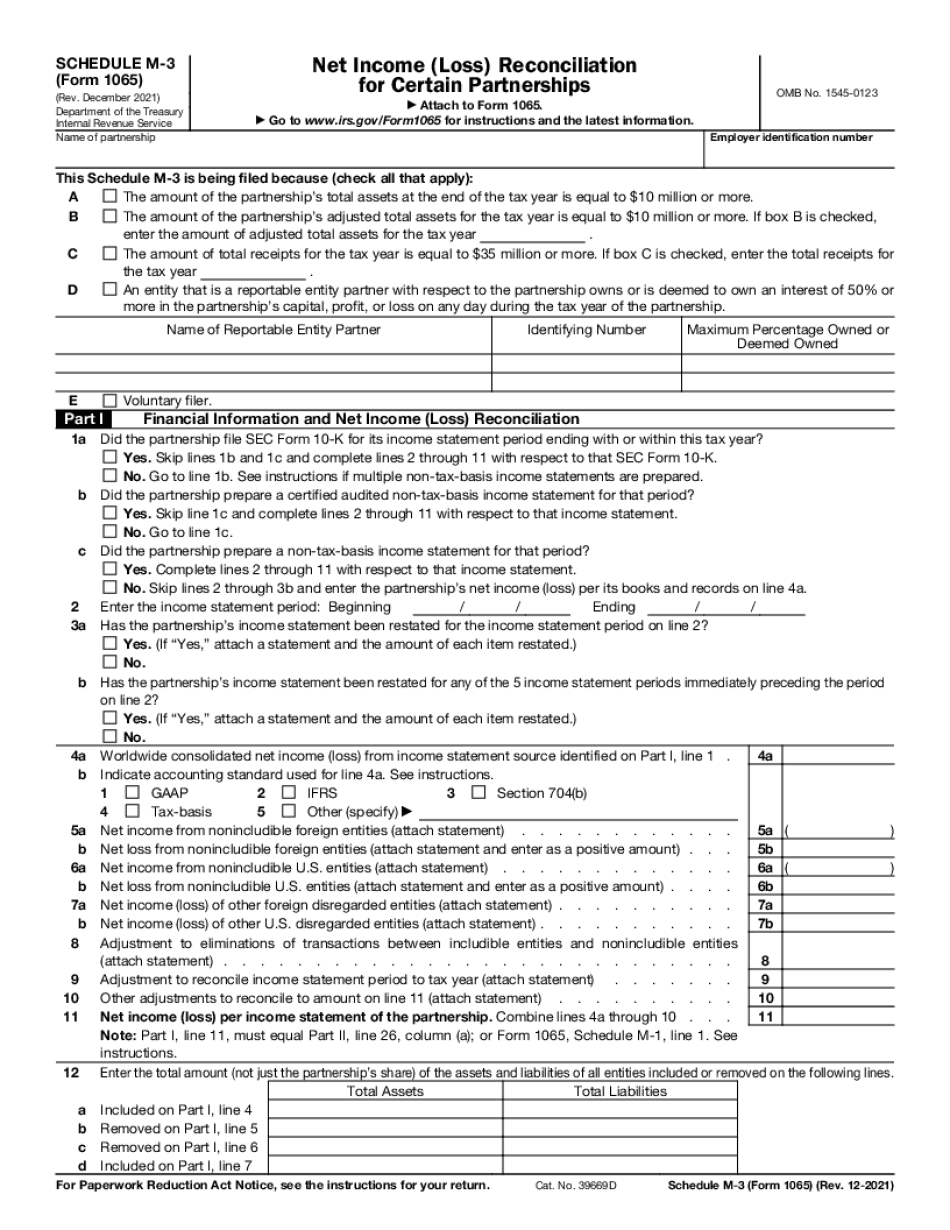

Video instructions and help with filling out and completing What Form 1065 Schedule M 3 Penalties