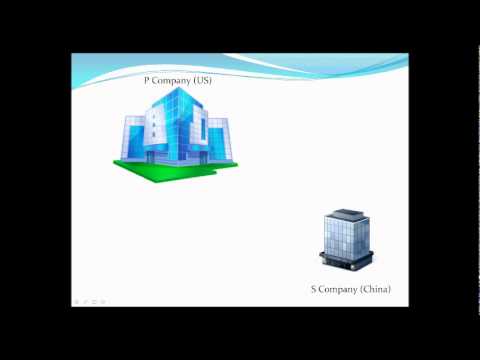

This is a presentation on booked attacks, permanent and temporary differences between a U.S. parent corporation and its foreign subsidiaries. We'll start by looking at the financial effects of a U.S. parent company assuming that it owns one hundred percent of the foreign subsidiary. We will discuss how they account for this investment in their books by using the equity method. Next, we'll explain the tax consequences of having a permanent reinvestment of foreign earnings. Then, we'll introduce an example of a temporary difference that could occur when intercompany transactions take place between the US parent corporation and the foreign corporation. We'd like to start with an example of a US parent corporation with its own foreign subsidiary in China. Assume that throughout the year, the foreign subsidiary had a net income of $2.5 million US dollars and they paid $100,000 in dividends to the US parent. Now, how would these amounts be reflected in the US parent's books? First of all, the moment the US parent acquired the foreign subsidiary, the US corporation had to create an investment account in the foreign subsidiary and debit that account by the acquisition price, which in our case was $4 million dollars. Also, let's assume the US parent chose to record its foreign subsidiary's transactions under the equity method. Therefore, if the foreign subsidiary had $2.5 million dollars in net income, the parent would record an increase in the investment in sub-account by debiting it by that amount and crediting equity in the foreign subsidiary to reflect the effect of an increase in earnings. If the foreign sub pays out a dividend of $100,000 to the parent Corp, the US parent Corp would debit cash and credit the investment in the foreign sub to reflect a decrease in the value of the...

Award-winning PDF software

Schedule M 3 temporary differences Form: What You Should Know

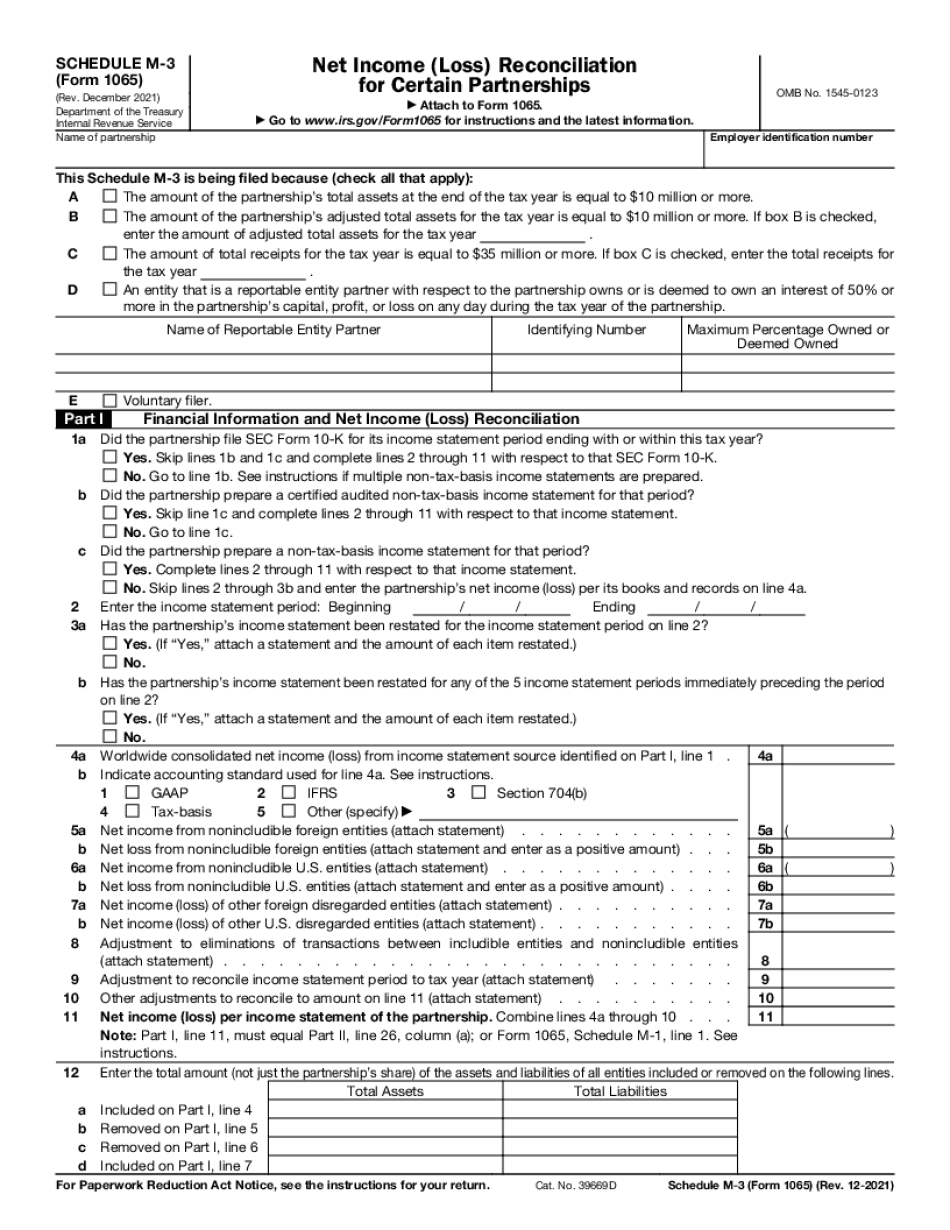

Instructions for Schedule M-3 (Form 1065) (Rev) The reconciliation totals for book, temporary difference, permanent difference, and taxable income for each subgroup are reported on Form 1120, page 3, which is Instructions for Form 1065 (Rev) December 22, 2024 — The taxpayer is to adjust the reconciliation totals for certain categories based on the amount of any temporary differences reported on Schedule M-3.

online solutions help you to manage your record administration along with raise the efficiency of the workflows. Stick to the fast guide to do Form 1065 (Schedule M-3), steer clear of blunders along with furnish it in a timely manner:

How to complete any Form 1065 (Schedule M-3) online: - On the site with all the document, click on Begin immediately along with complete for the editor.

- Use your indications to submit established track record areas.

- Add your own info and speak to data.

- Make sure that you enter correct details and numbers throughout suitable areas.

- Very carefully confirm the content of the form as well as grammar along with punctuational.

- Navigate to Support area when you have questions or perhaps handle our assistance team.

- Place an electronic digital unique in your Form 1065 (Schedule M-3) by using Sign Device.

- After the form is fully gone, media Completed.

- Deliver the particular prepared document by way of electronic mail or facsimile, art print it out or perhaps reduce the gadget.

PDF editor permits you to help make changes to your Form 1065 (Schedule M-3) from the internet connected gadget, personalize it based on your requirements, indicator this in electronic format and also disperse differently.

Video instructions and help with filling out and completing Schedule M 3 temporary differences