Music - how are distributions from a limited partnership position and apartment syndication taxed? I love these concepts that seem simple, but then I realize that there is more to it. I recently had an experience with someone regarding this. What they did was, if you were a limited partner, meaning you were not actively participating and not at risk, in a lot of apartment syndications, they would tell you to invest $100,000 and promise to give you back not only your initial investment within a year, but also additional profit. And the catch is, they would distribute a portion of the profit by fixing up the apartment and refinancing it. This way, they distribute cash and you receive your money back tax-free. So basically, if I have a capital account, I can always get my investment back tax-free. However, if there is a loss, I am limited in using that loss as a limited partner, unless I am at risk. If I have income, regardless of other factors, I have to pay taxes on that income. For example, if I receive a K1 form that shows income, I have to pay taxes on that income. On the other hand, if I receive back more cash than I initially invested and I don't have enough basis or risk, it is considered long-term capital gains. This is quite strange. Typically, in apartment syndications, the promoter would inform investors that they need $500,000 from the investment pool to fix up an apartment. They would have financing for the rest of the expenses and expect to receive a significant amount of cash once the project is completed. This is known as the "buy, rehab, rent, refinance" model. After receiving the cash, they would issue it to the owners. So, if you invested $100,000...

Award-winning PDF software

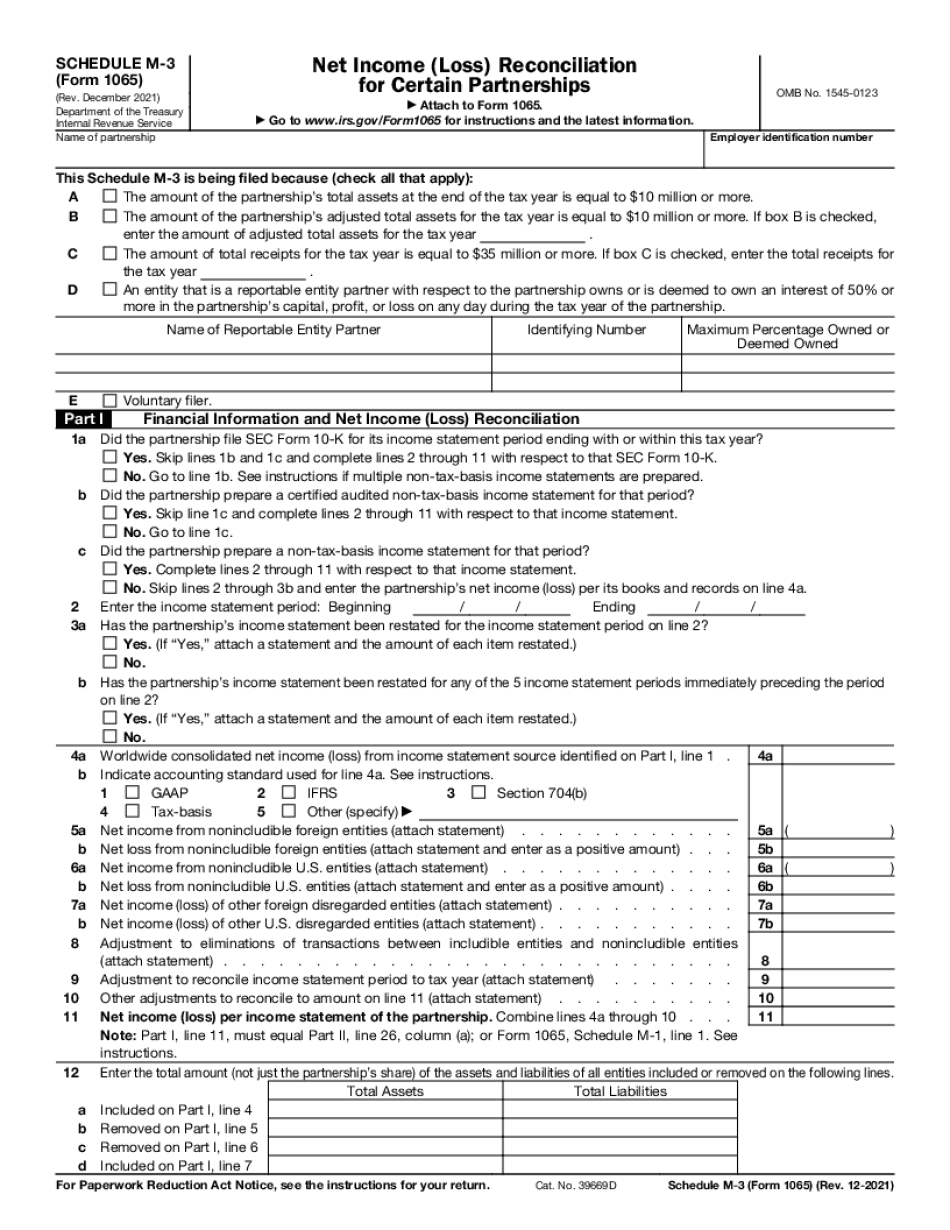

Reportable entity partner Form: What You Should Know

How Long To Wait After a Reportable Entity Partner Leaves to File Your Taxes on Schedule M-3? Dec 15, 2024 — The deadline for a reportable entity partner to file Form 1065 should be at the last day of the calendar year following the end of its period of ownership, but not later than the last day of the calendar year in which it was created. For more information, see Section 716(c) and the Instructions for Schedule M-3. Entities Who Are Not Partners May Needs To File Taxes on 1065 Jan 11, 2024 — If a partnership does not file a Schedule M-3 or its partner(s) does not file 1065, it may not be entitled to a partnership tax distribution. To get your distribution, you need to file Form 8916 with your federal income tax return and attach any required Forms 1065/M-3 on both the 1065 and 8916 forms. What Is the New Schedule M-3? The schedule M-3, also known as “Form 1065”, is an annual schedule that must be filed with all tax returns and financial statements by any company that owns more than 50% of a company's profit, loss, or capital. Filing Form 1065 Schedule 1065 (Partnerships) Schedule M-3 Schedule M-3 (Partnerships) Form 1065 and Tax Information Statement (Form 1065-B) (12/11/2016) — Internal Revenue Service Filing Schedule M-3 (Partnerships) (10/23/2017) — Internal Revenue Service Why Do You Need To File Schedule M-3 For Partnerships? Entities need to file Schedule M-3 if they own more than 50% of a partnership's profits, losses, or capital. (The partnership tax rules require that partnership partners must report and pay tax on any partnership or partnership interests that could potentially be related.) To help illustrate this, we have included the following examples to illustrate how to calculate the appropriate amount to report on your 1065 and to file Form 8916 with your federal income tax return. Example #1: Example 1 is not applicable to partnership distributions, but shows the basic principle. If a corporation (called The Partnership) owned 10% of your corporation's profits, and there were no other restrictions or requirements, the partnership needs to report and pay tax on all net (losses plus gains) income.

online solutions help you to manage your record administration along with raise the efficiency of the workflows. Stick to the fast guide to do Form 1065 (Schedule M-3), steer clear of blunders along with furnish it in a timely manner:

How to complete any Form 1065 (Schedule M-3) online: - On the site with all the document, click on Begin immediately along with complete for the editor.

- Use your indications to submit established track record areas.

- Add your own info and speak to data.

- Make sure that you enter correct details and numbers throughout suitable areas.

- Very carefully confirm the content of the form as well as grammar along with punctuational.

- Navigate to Support area when you have questions or perhaps handle our assistance team.

- Place an electronic digital unique in your Form 1065 (Schedule M-3) by using Sign Device.

- After the form is fully gone, media Completed.

- Deliver the particular prepared document by way of electronic mail or facsimile, art print it out or perhaps reduce the gadget.

PDF editor permits you to help make changes to your Form 1065 (Schedule M-3) from the internet connected gadget, personalize it based on your requirements, indicator this in electronic format and also disperse differently.

Video instructions and help with filling out and completing Reportable entity partner